Introduction

As the Government of Oman has announced the latest implementation of the VAT in business deals across the country, various business organizations are being pushed to adopt new and advanced Tax embedded business transaction technologies. Which has become the most important need of the hour!

Preparing for VAT!

The 3-phase process

Phase 1: Impact assessment

- Perform detailed analysis of end to end business transaction flows (GAP analysis)

- Perform walkthrough of the sales/accounts receivable cycle and purchases/accounts payable cycle and identify VAT-risk areas

- Mapping transaction for VAT enablement (tax mapping)

- Review contracts and identify the VAT impact

- Provide report on VAT compliance needs

Phase 2: VAT Implementation and training

- Review existing IT systems and assess their suitability for VAT enablement

- Review system design and monitor the implementation of the recommended change to IT systems

- Work with the in-house IT team/Vendors to finalize and identify the customizations /configurations necessary to be made to the IT system to ensure that system meets Oman VAT law requirements

- Review credit policies and advise on cash flow management and inventory management related areas

- Conduct a function-specific VAT workshop to personnel in preparation to meet the VAT compliance obligations

Phase 3: Compliance Assistance

- Assist in VAT registration

- Guidance on first VAT Return filing and related documentation

- Provide periodic VAT updates

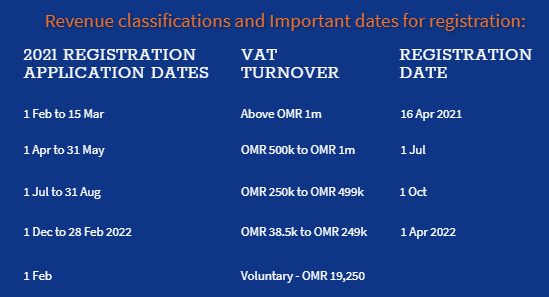

Deadlines and Turnover limits for VAT registration

SOME IMPORTANT OMAN GOV. WEBSITE LINKS FOR VAT QUERIES

VAT Registration Application – For Resident no CRN

VAT Registration Application – For Non Resident

VAT Registration Manual Guide – Persons with CRN

How to Print/Issue VAT Certificate

How to Update VAT Registration Application

Oman VAT ID Number Validity Verification Link

VAT Law English Translation

VAT Regulation unofficial English version

VAT – Business – FAQ

Determining Food Items subject to Value Added Tax at Zero Rate

Impact on Retail and Restaurant businesses

Let us look into some of the most prevalent scenarios in Oman to understand the VAT implications 👇🏻

Discounts

One of the most traditional sale strategy is ‘discounts’ where the customer is benefited by reduction in price. Now the question which retailers will have is; will VAT be charged on the value after considering the discount or on the full value of supply without considering the discount? Practically, VAT should be collected on the discounted price paid by the customer.

Bundle Offer

In the case of ‘bundle offer’ given by retailers like buy one get one free or buy three for RO 10, a single consideration is received from the customer and will be construed as the consideration for all the items sold and accordingly VAT will be applied. The key challenge foreseen for retailers here will be how the tax invoice will disclose the same, how the pricing in the product master will accommodate the offer and how the accounting module will be redesigned to reflect correct VAT treatment. Though this may look gimmick to retailers but as Oman has only two VAT rates 5% and 0%, there will not be many complication as in case of pick-n-mix bundle offer prevalent in other sales tax regimes around the globe with multiple tax rates over products.

Free Gifts!

In the case of ‘free gifts’ offered by retailers like shop worth RO 20 and get a pack of 10 masks free, the question is how will the free item be treated for VAT purpose. The Executive Regulation will most likely exempt low value items from being treated as deemed supply. However, anything above the stated limit with be subject to VAT. That means VAT is not collected from the customer as the items is given for free but VAT liability exists for the retailer and is to be paid to the Tax Authorities. This is something which should alert retailer as to how the accounting modules will be automated to account VAT correctly for an item with zero sale price.

Loyalty Programs

Big international retail-chains, hotels and airlines have loyalty programs or cards mainly to boost repetitive sales. Will those be subject to VAT? Automobile dealers offer free service and offer free accessories on vehicle sales. How the same will be treated for VAT? Many time corporates give gifts to their employees on which they have claimed input credit. What will the VAT impact on such transactions?

Solution!

An effective VAT embedded POS Software/ERP in Oman and Muscat can also help to manage all your accounts and records after paying or deducting taxes. It can also help you to manage critical business requirements and simplify the business processes easily and effectively.

It is the need of the hour for all business partners in Oman to maintain and manage their accounts by VAT embedded efficient ERP/POS software systems that can handle all the decisions related to the business. So that they can save time and help businesses to flourish effectively and efficiently.

Goods and Services under VAT 5

All goods and services bought or sold or imported into the Sultanate of Oman are subject to VAT and a standard rate of 5% VAT will be levied on all such supplies. The businesses registered under Oman VAT are responsible to levy VAT @ 5% on such supplies, collect it from their customers and remit it to the government.

Goods and Services under VAT 0

- Notified supply of food items.

- Supply of medicines and medical equipment as notified by the authorities.

- Supply of investment gold, silver, and platinum.

- Supplies of international and intra GCC transport of goods or passengers.

- Supply of services in connection with this transport.

- Supply of air, sea, and land means of transport that is designated for the transportation of passengers and goods for commercial purposes and the supply of Goods and Services related to transport.

- The supply of rescue planes, and rescue and assistance boats

- The supply of oil, oil derivatives, and natural gas

- Supplies made to outside the GCC territory as mentioned below:

- Export of goods.

- Supply of goods or services to or within one of the customs duty suspension cases mentioned in the Common Customs Law.

- Re-export of goods that have been temporarily imported to Oman for repair, refurbishment, conversion or processing, and services added to it.

- Supply of services by a taxable Supplier that has a place of residence in the Sultanate to a Customer that does not have a place of residence in the GCC States, barring few that is notified in the law.

- Supply of goods or services that are exempt from tax in the sultanate and that are supplied to outside of the GCC states.

- Supplies of goods and services from to or within special economic zones

Goods and Services under VAT Exempt

The following are supplies that are exempt from the VAT. It is important to note that specific conditions and guidelines will be issued in executive regulations pertaining to supplies listed below.

- Financial Services.

- Healthcare Services and related Goods and Services.

- Educational Services and related Goods and Services.

- Undeveloped land (bare land).

- Resale of residential properties.

- Local passenger transport.

- Rental of properties for residential purposes

List of goods import supplies that are exempt under Oman VAT

- Imported Goods in cases where the supply of such Goods is exempted from Tax or subject to Tax at a rate of zero percent in the destination point of entry.

- Imported Goods in favor of diplomatic and consular Bodies, and international organizations, and to Heads and members of consular and consular bodies certified by the Sultanate, on the condition of reciprocity.

- Anything imported to the armed forces and internal security forces in all its divisions such as ammunition, weapons, supplies, and military means of transport and its parts.

- Personal effects and used household appliances brought by citizens residing abroad and foreigners who are coming to stay in the country for the first time.

- The supplies for non-profit charities.

- Returned Goods

Exemption in case of baggage and gifts

Personal baggage and gifts accompanying travelers arriving in the sultanate, and requisites for people with special needs are exempt from Tax. These will be exempted only when the specific conditions and rules mentioned in the regulations are met.

Broadly, VAT exemptions in Oman are given for certain financial services, re-sale residential buildings, supply of bare land, local passengers, etc. However, to consider a supply as exempted from the VAT, the specific conditions mentioned in the Oman VAT Act and Executive Regulations need to be fulfilled.

How does Saleculator help?!

We at Saleculator provide a unique solution for retailers, restaurants, and other business partners with an effective VAT-enabled POS system. Amplify your Business with Saleculator POS by easy billing Software and effortless flow of Retail business with our perfect Hybrid (Both cloud and offline) based POS Software to improve your sales, inventory tracking, multi-store management to boost your profit, and easy business transaction with secured POS System in Oman and overseas.

Looking for customization of your retail, restaurant POS with upcoming VAT Implementation? Contact our technical team for a quick Demo for a fully-featured VAT Enabled POS System in Oman.